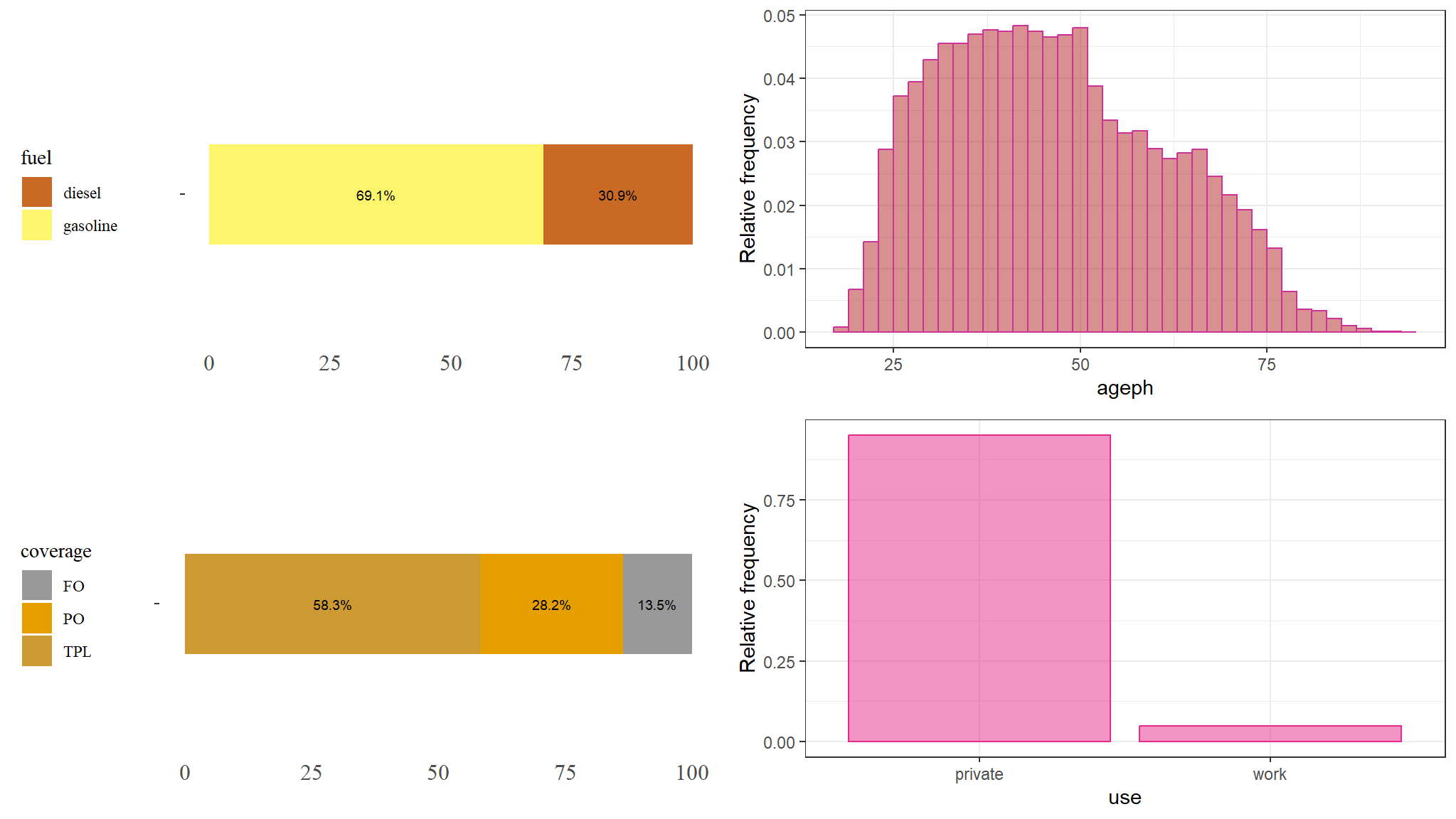

| ID | NCLAIMS | AMOUNT | AVG | EXP | COVERAGE | FUEL | USE | FLEET | SEX | AGEPH | BM | AGEC | POWER | PC | TOWN | LONG | LAT |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 1 | 1618.001 | 1618.001 | 1.000 | TPL | gasoline | private | N | male | 50 | 5 | 12 | 77 | 1000 | BRUSSEL | 4.355 | 50.845 |

| 2 | 0 | 0.000 | NA | 1.000 | PO | gasoline | private | N | female | 64 | 5 | 3 | 66 | 1000 | BRUSSEL | 4.355 | 50.845 |

| 3 | 0 | 0.000 | NA | 1.000 | TPL | diesel | private | N | male | 60 | 0 | 10 | 70 | 1000 | BRUSSEL | 4.355 | 50.845 |

| 4 | 0 | 0.000 | NA | 1.000 | TPL | gasoline | private | N | male | 77 | 0 | 15 | 57 | 1000 | BRUSSEL | 4.355 | 50.845 |

| 5 | 1 | 155.975 | 155.975 | 0.047 | TPL | gasoline | private | N | female | 28 | 9 | 7 | 70 | 1000 | BRUSSEL | 4.355 | 50.845 |

| 6 | 0 | 0.000 | NA | 1.000 | TPL | gasoline | private | N | male | 26 | 11 | 12 | 70 | 1000 | BRUSSEL | 4.355 | 50.845 |

Modeling Claim frequency

Offsetting

generalized linear models

insurance

Background

Modeling claim frequency using GLMS

Offsets in Poisson models explained

- In some applications, the linear predictor contains a term that requires no estimation, which is called an

offset. - The offset can be viewed as a term \(\beta_jx_{ji}\) in the linear predictor for which \(\beta_j\) is known a priori.

- For example, consider modelling the annual number of hospital births in various cities to facilitate resource planning. The annual number of births is discrete, so a Poisson distribution may be appropriate.

- However, the expected annual number of births \(\mu_i\) ,in city i depends on the given populations \(P_i\) of the city, since cities with larger population would be expected to have more births each year, in

- The number of births per unit of population, assuming a logarithmic link function, can be modelled using the systematic component \(\log(\frac{\mu}{P}) = \phi\),for the linear predictor \(\phi\).

- Rearranging to model \(\mu\): \[log(\mu) = log P + \phi\]. in more mathematical terms the model without an offset is as follows

\[E(Y|X)=e^{\theta^T}x\] which simplifies to \[log(E|X)=\theta^Tx\]

while the model with an offset is given by :

\[E(Y|X)=e^{\theta^T}x*S_i\] which simplifies to \[log(E|X)=\theta^Tx+logS_i\]

- The first term in the systematic component log P is completely known: nothing needs to be estimated. The term log P is called an offset. Offsets commonly appear in Poisson glms, but may appear in any glm.

- The offset variable is commonly a measure of exposure. For example, the number of cases of a certain disease recorded in various mines depends on the number of workers, and also on the number of years each worker has worked in the mine.

- The exposure would be the number of person-years worked in each mine, which could be incorporated into a glm as an offset. That is, a mine with many workers who have been employed for many years would be exposed to a greater likelihood of a worker contracting the disease than a mine with only a few workers who have been employed for short periods of time.

Introduction

- in this analysis we have variables such as

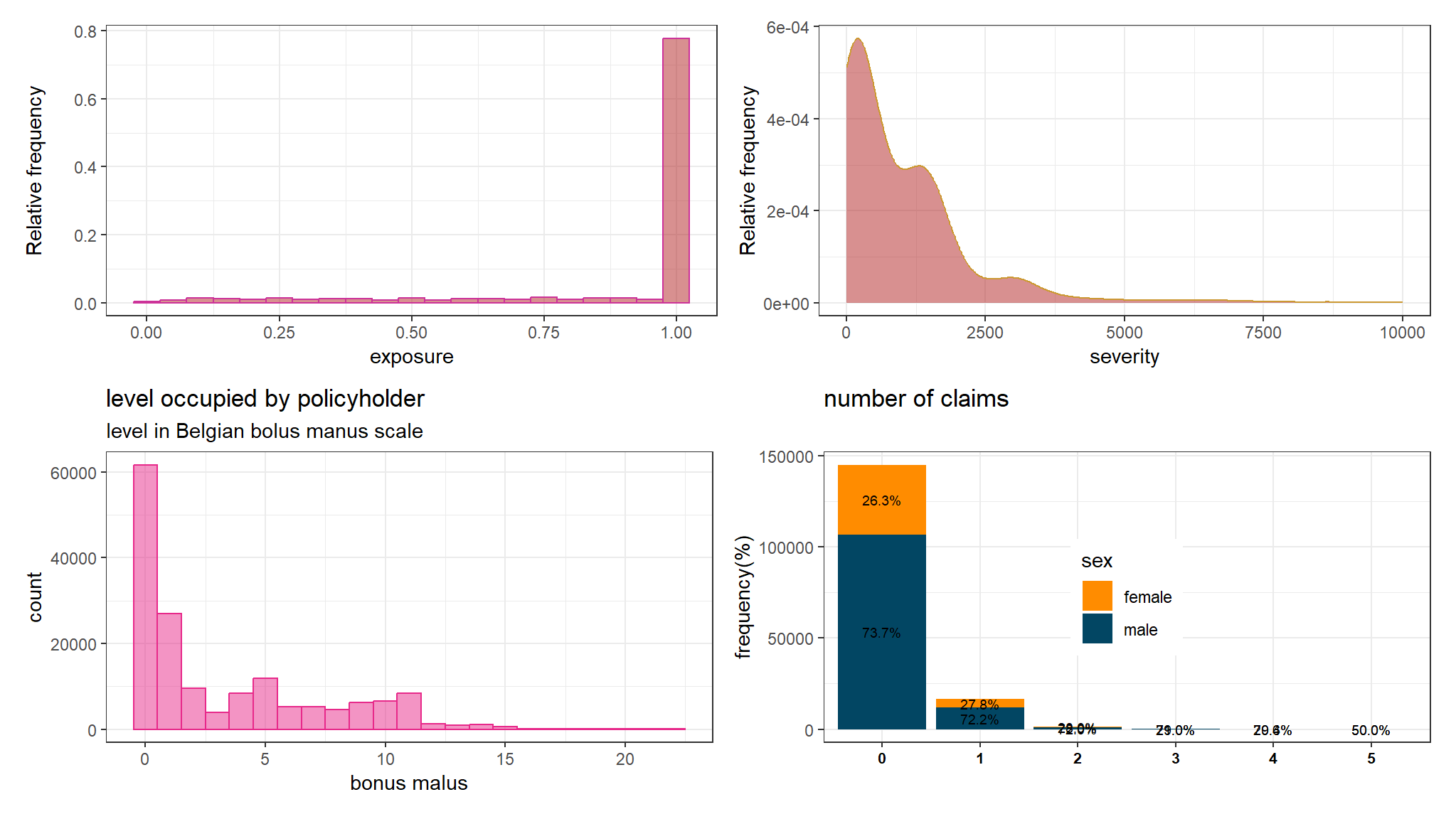

number of claims,severityandexposure - we intend to model severity as well as

number of claims per unit exposure - In this article the term exposure is a measure of what is being insured. Here an insured vehicle is an exposure. If the vehicle is insured as of July 1 for a certain year, then during that year, this would represent an exposure of 0.5 to the insurance company.

data Exploration

- define a function to rename the variables to lower case

- rename

exptoexposure

out_dat <- out_new %>%

rename_all(function(.name) {

.name %>%

tolower

})

out_dat <-out_dat |>

rename(exposure = exp)explore the dataset

- what variables do we have?

names(out_dat)

#> [1] "id" "nclaims" "amount" "avg" "exposure" "coverage"

#> [7] "fuel" "use" "fleet" "sex" "ageph" "bm"

#> [13] "agec" "power" "pc" "town" "long" "lat"- what are the data types

#> id nclaims amount avg exposure coverage

#> "integer" "integer" "numeric" "numeric" "numeric" "character"

#> fuel use fleet sex ageph bm

#> "character" "character" "character" "character" "integer" "integer"

#> agec power pc town long lat

#> "integer" "integer" "integer" "character" "numeric" "numeric"- change to character to factor variables!

out_dat<-out_dat |>

mutate_if(is.character,as.factor)Explanatory analysis

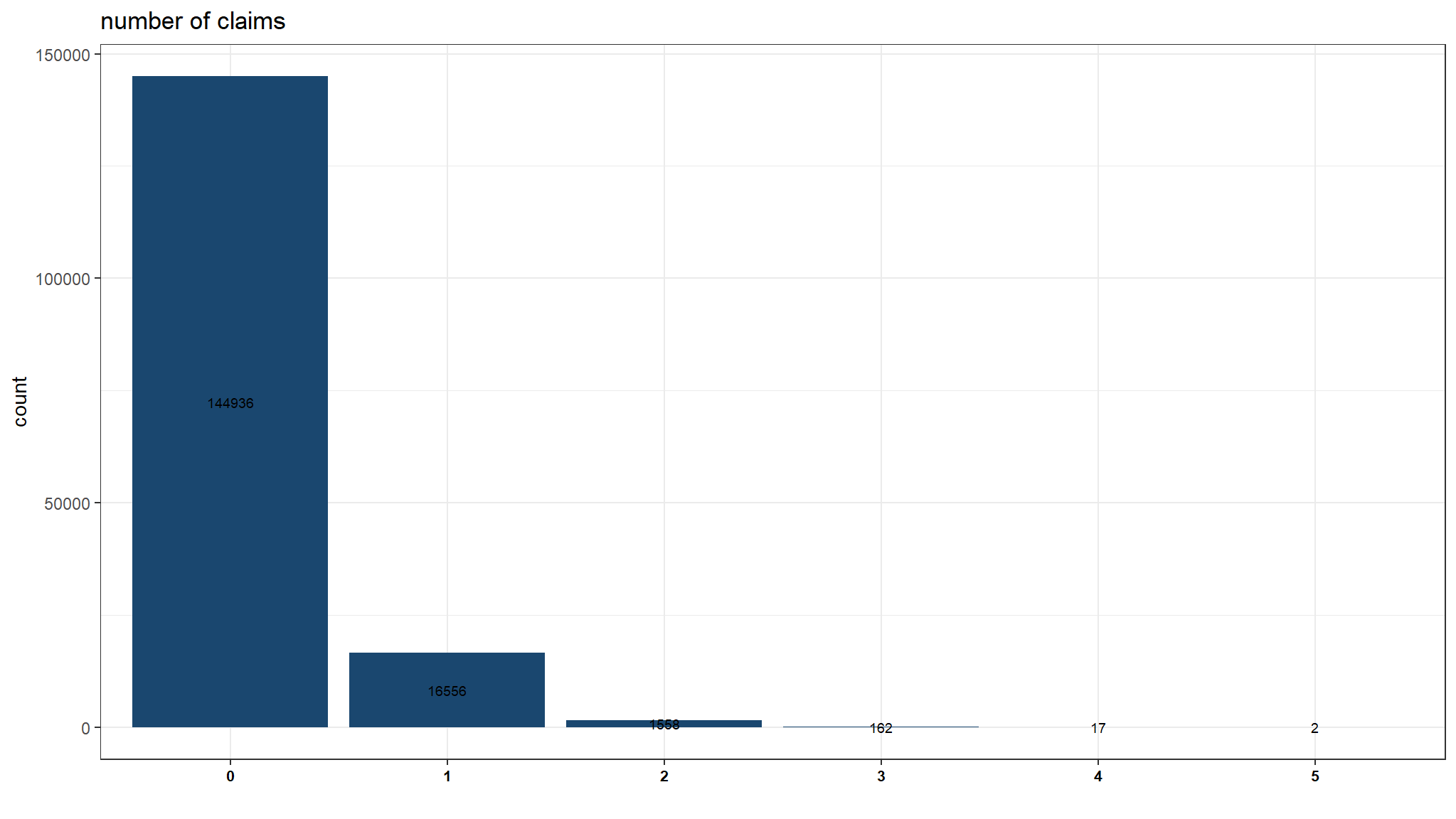

explore number of claims (our target variables)

plot_data<-out_dat |>

group_by(nclaims) %>%

tally() |>

mutate(variable="variable",

nclaims=as.factor(nclaims))

g1 <- ggplot(plot_data, aes(x=nclaims,y=n,fill=variable)) +

theme_bw() +

geom_col() +

geom_text(aes(label=n),position=position_stack(vjust=0.5),size=2.5)+

labs(title = "number of claims", y = "count", x ="",fill="") +

ggthemes::scale_fill_stata() +

theme(legend.position = "none",

axis.text.x = element_text(face="bold",

color="black",

size=8))

g1

Note

- number of claims is

descrete(count) in nature and it can be noted that this cannot follow a normal distribution - the data is right skewed

- for this reason we model using a generalized linear model (poisson to be frank)

The Poisson distribution

- it specifies the probability of a discrete random variable \(Y\) and is given by:

\[f(y, \,\mu)\, =\, Pr(Y = y)\, =\, \frac{\mu^y \times e^{-\mu}}{y!}\]

\[E(Y)\, =\, Var(Y)\, =\, \mu\]

where \(\mu\) is the parameter of the Poisson distribution

The Poisson distribution is particularly relevant to model count data because it:

- specifies the probability only for integer values

- \(P(y<0) = 0\), hence the probability of any negative value is null

- \(Var(Y) = \mu\) (the mean-variance relationship) allows for heterogeneity (e.g. when variance generally increases with the mean)

lets see if the above conditions are close

out_dat |>

summarise(variance=var(nclaims),

average = mean(nclaims),

`emperical frequency(total claims/total exposure)` = sum(nclaims) / sum(exposure),

var =sum((nclaims -`emperical frequency(total claims/total exposure)` * exposure)^2)/sum(exposure)) |>

gather(key="statistic",value = "values") |>

knitr::kable(digits=3, "html", caption="Table 1: variance and mean are almost equal hence a poisson fits well") %>%

kable_styling("striped", "bordered") | statistic | values |

|---|---|

| variance | 0.135 |

| average | 0.124 |

| emperical frequency(total claims/total exposure) | 0.139 |

| var | 0.152 |

Note

-

variance is almost equal to the averagehence we can really see a poisson model works well here - the value

varis still \(Var(Y)=E[(Y-E(Y))^2]\) were we empirically calculate the first expected value by taking exposure into account. - we then compare each realization of

nclaimswith its expected value i.em*expowhere m is the global empirical claim frequency

Risk classification for gender category

out_dat %>%

group_by(sex) %>%

summarise(`emperical frequency` = sum(nclaims) / sum(exposure),

`total claims`=sum(nclaims),

count=n()) |>

knitr::kable(digits=3, "html", caption="Table : summary by gender") %>%

kable_styling("striped", "bordered") | sex | emperical frequency | total claims | count |

|---|---|---|---|

| female | 0.148 | 5634 | 43175 |

| male | 0.136 | 14602 | 120056 |

Note

- both males and females have almost the same average

emperical frequency - There were many more claims by men, although there were more men in the data. The simplest approach to analyzing these data would be to do a two-sample comparison using the

poisson.test()function . It requires the counts for one or two groups.

For our application, the hypotheses to compare the two sexes are:

\[\begin{align} H_0&: \lambda_m = \lambda_f \notag \\ H_a&: \lambda_m \ne \lambda_f \notag \end{align}\]poisson.test(c(120056 , 43175), T = 3)#>

#> Comparison of Poisson rates

#>

#> data: c(120056, 43175) time base: 3

#> count1 = 120056, expected count1 = 81616, p-value < 2.2e-16

#> alternative hypothesis: true rate ratio is not equal to 1

#> 95 percent confidence interval:

#> 2.750243 2.811500

#> sample estimates:

#> rate ratio

#> 2.780683

Note

The function reports a p-value as well as a confidence interval for the ratio of the claim rates. The results indicate that the observed difference is greater than the experiential noise and favors \(H_a\).

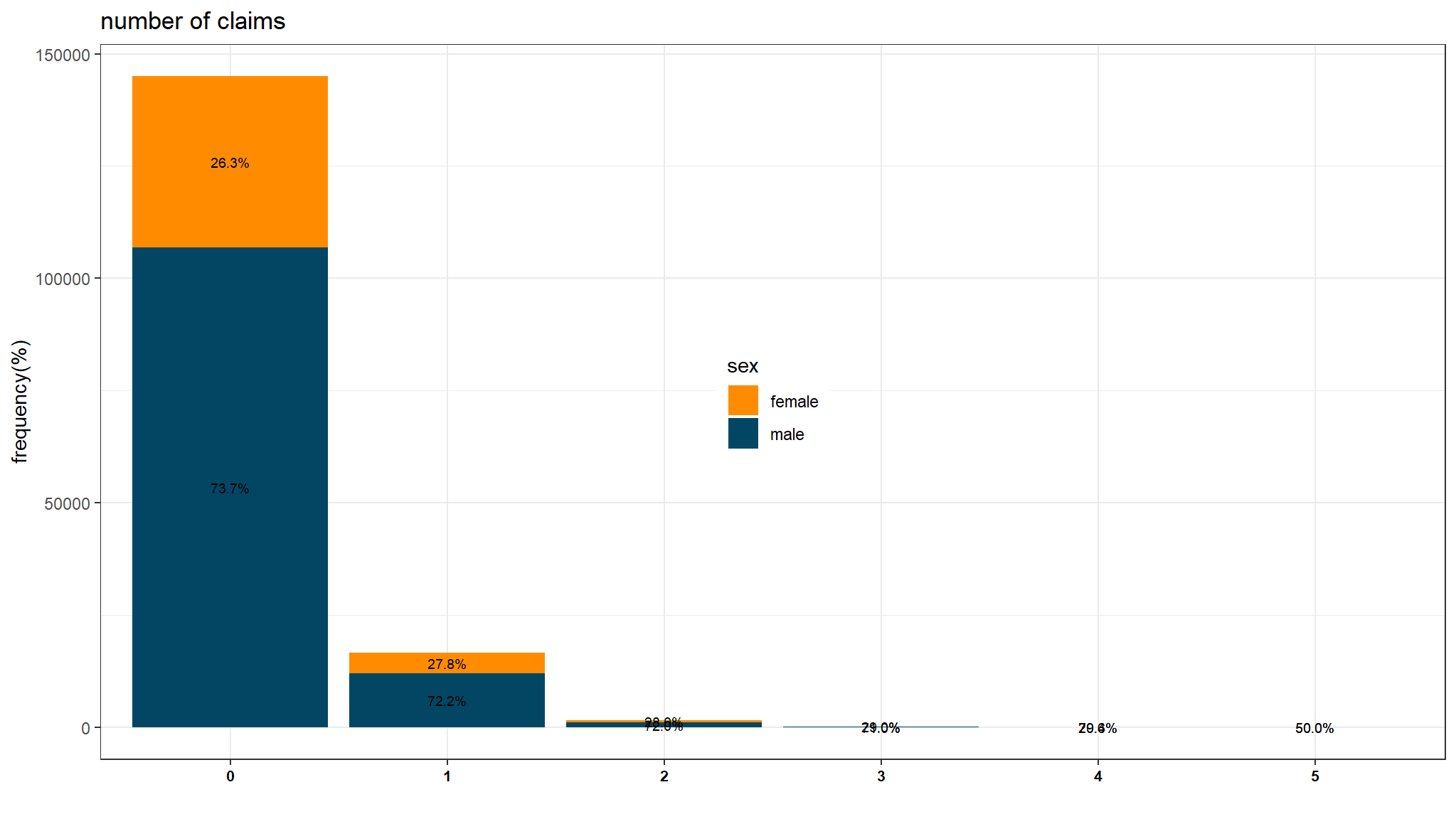

Relative frequency of claims

plot_data<-out_dat |>

group_by(nclaims,sex) |>

tally() |>

mutate(pct = n/sum(n)*100,

lbl = sprintf("%.1f%%", pct)) |>

mutate(variable="variable",

nclaims=as.factor(nclaims))

g2 <- ggplot(plot_data, aes(x=nclaims,y=n,fill=sex)) +

theme_bw() +

geom_col() +

geom_text(aes(label=lbl),position=position_stack(vjust=0.5),size=2.5,)+

labs(title = "number of claims", y = "frequency(%)", x ="",fill="sex") +

tvthemes::scale_fill_kimPossible() +

theme(legend.position = c(0.5, 0.5),

axis.text.x = element_text(face="bold",

color="black",

size=8))

g2

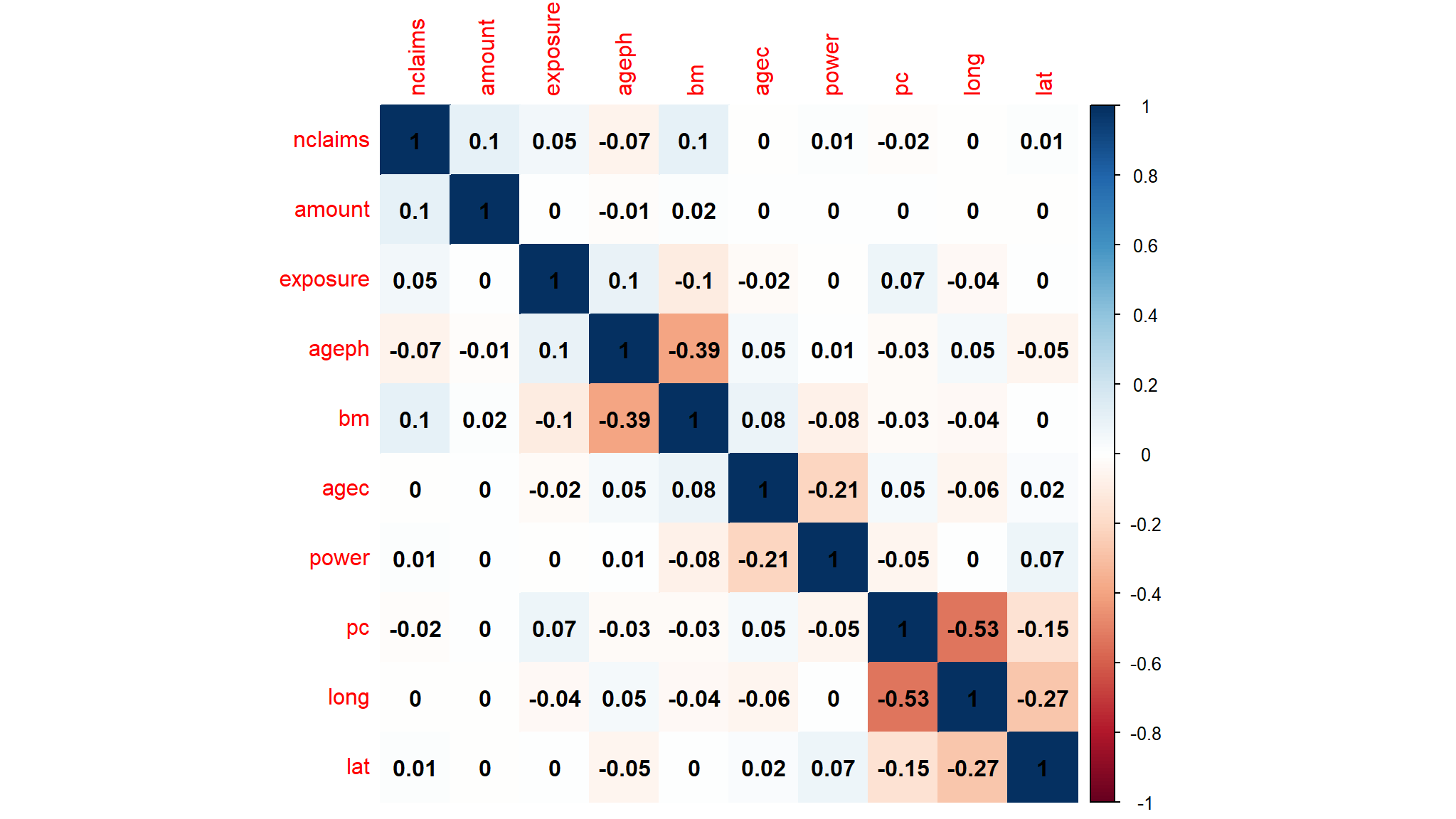

Further exploration

correlation

CALIBRATING A simple GLM

- like we said before , we need to include the

exposurevariable being offsetted hence we defineoffset=log(exposure)

Trivial model (null model)

#>

#> Call:

#> glm(formula = nclaims ~ 1, family = poisson(link = "log"), data = out_dat,

#> offset = log(exposure))

#>

#> Coefficients:

#> Estimate Std. Error z value Pr(>|z|)

#> (Intercept) -1.97087 0.00703 -280.4 <2e-16 ***

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#>

#> (Dispersion parameter for poisson family taken to be 1)

#>

#> Null deviance: 89944 on 163230 degrees of freedom

#> Residual deviance: 89944 on 163230 degrees of freedom

#> AIC: 127678

#>

#> Number of Fisher Scoring iterations: 6a model with sex variable

#>

#> Call:

#> glm(formula = nclaims ~ sex, family = poisson(link = "log"),

#> data = out_dat, offset = log(exposure))

#>

#> Coefficients:

#> Estimate Std. Error z value Pr(>|z|)

#> (Intercept) -1.90763 0.01332 -143.186 < 0.0000000000000002 ***

#> sexmale -0.08662 0.01568 -5.523 0.0000000333 ***

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#>

#> (Dispersion parameter for poisson family taken to be 1)

#>

#> Null deviance: 89944 on 163230 degrees of freedom

#> Residual deviance: 89914 on 163229 degrees of freedom

#> AIC: 127650

#>

#> Number of Fisher Scoring iterations: 6

what do we have

- generally the output suggests a model such as the following!

\[x'\beta =log(exposure)+\beta_0+\beta_1I(male)\] which when put otherwise simplifies to \[E(Y)=exposure*e^{(\beta_0+\beta_1I(male))}\]

we can also implement the same constraint using the function

weights=exposurethis should literally give the same results from the previous one with offset alone.

#>

#> Call:

#> glm(formula = nclaims/exposure ~ sex, family = poisson(link = "log"),

#> data = out_dat, weights = exposure)

#>

#> Coefficients:

#> Estimate Std. Error z value Pr(>|z|)

#> (Intercept) -1.90763 0.01332 -143.186 < 0.0000000000000002 ***

#> sexmale -0.08662 0.01568 -5.523 0.0000000333 ***

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#>

#> (Dispersion parameter for poisson family taken to be 1)

#>

#> Null deviance: 89944 on 163230 degrees of freedom

#> Residual deviance: 89914 on 163229 degrees of freedom

#> AIC: Inf

#>

#> Number of Fisher Scoring iterations: 6another interesting way is to use the tidymodels, took me loads of searching to come to thisyou literally need an additional package called

offsetregthen follow the following steps

out_dat$offset<-log(out_dat$exposure)glm_off<-poisson_reg_offset() |>

set_engine("glm_offset",offset_col="offset") |> #this would have been offset=log(exposure)

fit(nclaims ~ sex,data=out_dat)

glm_off |>

pluck("fit") |>

summary()#>

#> Call:

#> stats::glm(formula = formula, family = family, data = data, offset = offset)

#>

#> Coefficients:

#> Estimate Std. Error z value Pr(>|z|)

#> (Intercept) -1.90763 0.01332 -143.186 < 0.0000000000000002 ***

#> sexmale -0.08662 0.01568 -5.523 0.0000000333 ***

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#>

#> (Dispersion parameter for poisson family taken to be 1)

#>

#> Null deviance: 89944 on 163230 degrees of freedom

#> Residual deviance: 89914 on 163229 degrees of freedom

#> AIC: 127650

#>

#> Number of Fisher Scoring iterations: 6

Tip

- If \(\beta_j = 0\) then \(exp(\beta_j) = 1\) and \(\mu\) is not related to \(x_j\). If \(\beta_j > 0\) then \(\mu\) increases if \(x_j\) increases; if \(\beta_j < 0\) then \(\mu\) decreases if \(x_j\) increases.

lets tidy this a bit

| Characteristic | IRR1 | 95% CI1 | p-value |

|---|---|---|---|

| sex | |||

| female | — | — | |

| male | 0.92 | 0.89, 0.95 | <0.001 |

| 1 IRR = Incidence Rate Ratio, CI = Confidence Interval | |||

Note

This shows that the impact of each explanatory variable is multiplicative. being male decreases \(\mu\) by factor of exp( \(\beta_\text{sexMale}=0.92\) ) as compared to being female.

Q-square test on drop in deviance

anova(freq_glm_null,freq_glm_1,test="Chisq")

#> Analysis of Deviance Table

#>

#> Model 1: nclaims ~ 1

#> Model 2: nclaims ~ sex

#> Resid. Df Resid. Dev Df Deviance Pr(>Chi)

#> 1 163230 89944

#> 2 163229 89914 1 30.109 0.00000004085 ***

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Note

- H0 rejected in favor of more complex model H1

- a model with sex performs better than an empty (

null) model

attempt an LRT test

anova(freq_glm_null,freq_glm_1,test="LRT")

#> Analysis of Deviance Table

#>

#> Model 1: nclaims ~ 1

#> Model 2: nclaims ~ sex

#> Resid. Df Resid. Dev Df Deviance Pr(>Chi)

#> 1 163230 89944

#> 2 163229 89914 1 30.109 0.00000004085 ***

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

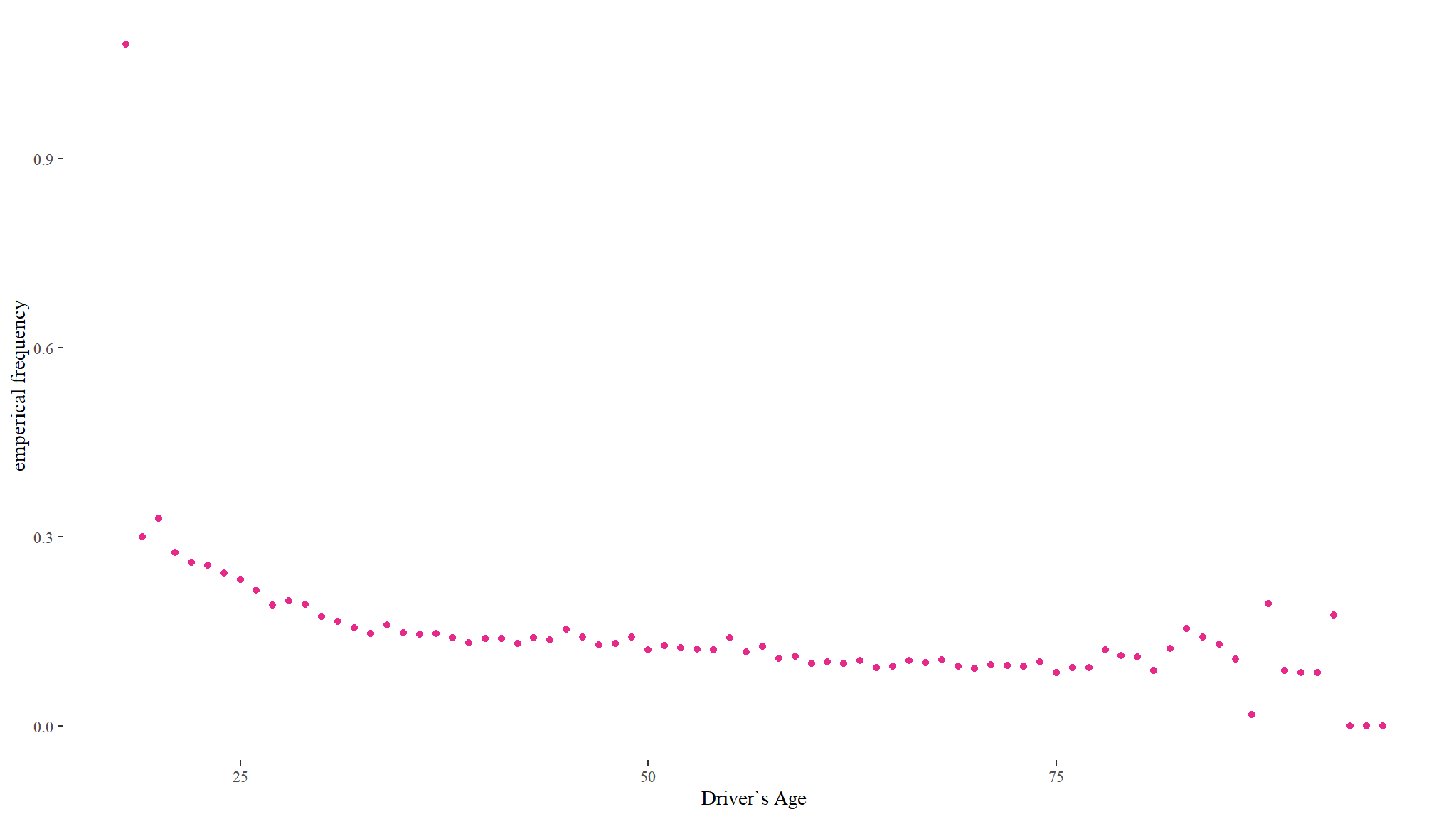

Emperical claim frequency as Driver age increases

out_dat %>%

group_by(ageph) %>%

summarise(`emperical frequency` = sum(nclaims) / sum(exposure),

total_clm=sum(nclaims)) %>%

ggplot(aes(x = ageph, y = `emperical frequency`)) +

theme_tufte() +

geom_point(color = ncube)+

labs(x="Driver`s Age")

Note

- the average driver’s age in the insurance portfolio is 47 years with ages ranging between 18 and 95

- the plot shows that the frequency of claims is significantly different between age groups with a peak at 18 years and then declining with increasing age .

Model age and predict

#>

#> Call:

#> glm(formula = nclaims ~ ageph, family = poisson(link = "log"),

#> data = out_dat, offset = log(exposure))

#>

#> Coefficients:

#> Estimate Std. Error z value Pr(>|z|)

#> (Intercept) -1.2286100 0.0229013 -53.65 <0.0000000000000002 ***

#> ageph -0.0162582 0.0004958 -32.79 <0.0000000000000002 ***

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#>

#> (Dispersion parameter for poisson family taken to be 1)

#>

#> Null deviance: 89944 on 163230 degrees of freedom

#> Residual deviance: 88829 on 163229 degrees of freedom

#> AIC: 126564

#>

#> Number of Fisher Scoring iterations: 6- tidy that up

| Characteristic | IRR1 | 95% CI1 | p-value |

|---|---|---|---|

| ageph | 0.98 | 0.98, 0.98 | <0.001 |

| 1 IRR = Incidence Rate Ratio, CI = Confidence Interval | |||

- Indeed , we see that the coefficient of

agewas negative and the resulting value less than 1 hence an increase in age decreases \(\mu\) - at

5%level of significance , age is a significant predictor of \(\mu\)

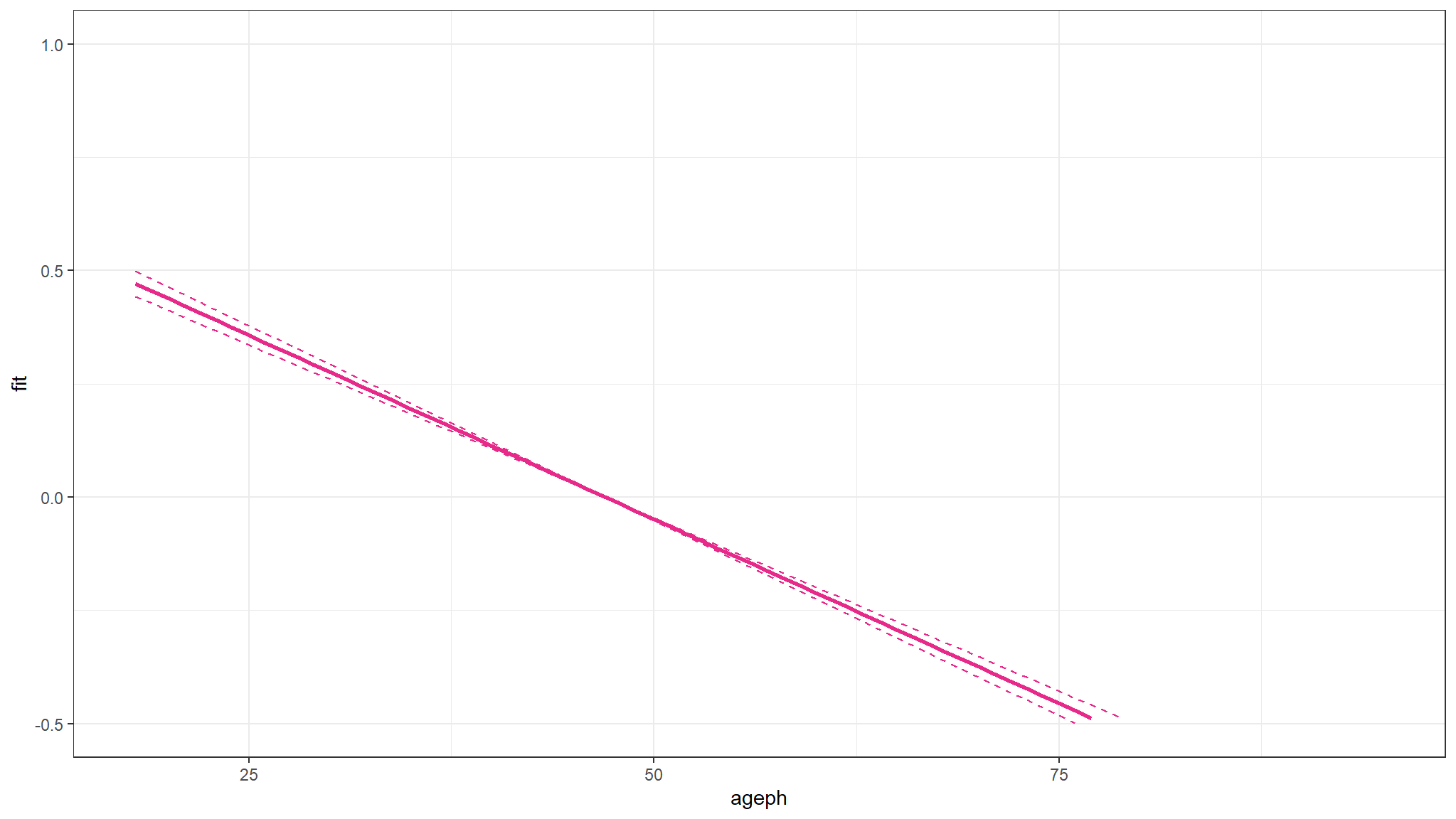

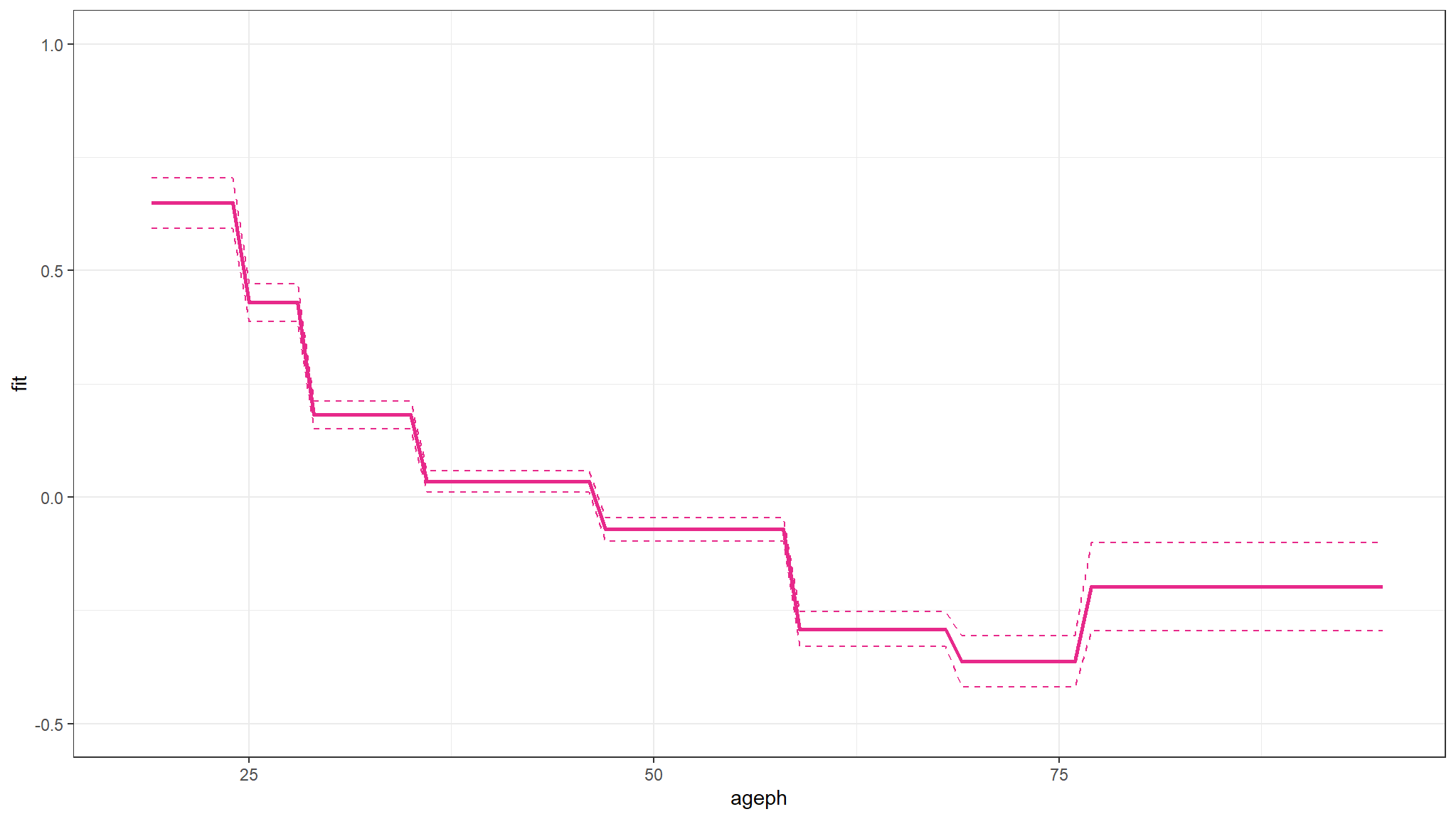

prediction

- lets do a prediction for ages in the range we already have but with an

expoureofone

a <- min(out_dat$ageph):max(out_dat$ageph)

pred_glm_age <- predict(freq_glm_age, newdata = data.frame(ageph = a, exposure = 1), type = "terms", se.fit = TRUE)

b_glm_age <- pred_glm_age$fit

l_glm_age <- pred_glm_age$fit - qnorm(0.975)*pred_glm_age$se.fit

u_glm_age <- pred_glm_age$fit + qnorm(0.975)*pred_glm_age$se.fit

df <- data.frame(a, b_glm_age, l_glm_age, u_glm_age)

Note

- expected \(\mu\) would also decrease with age .

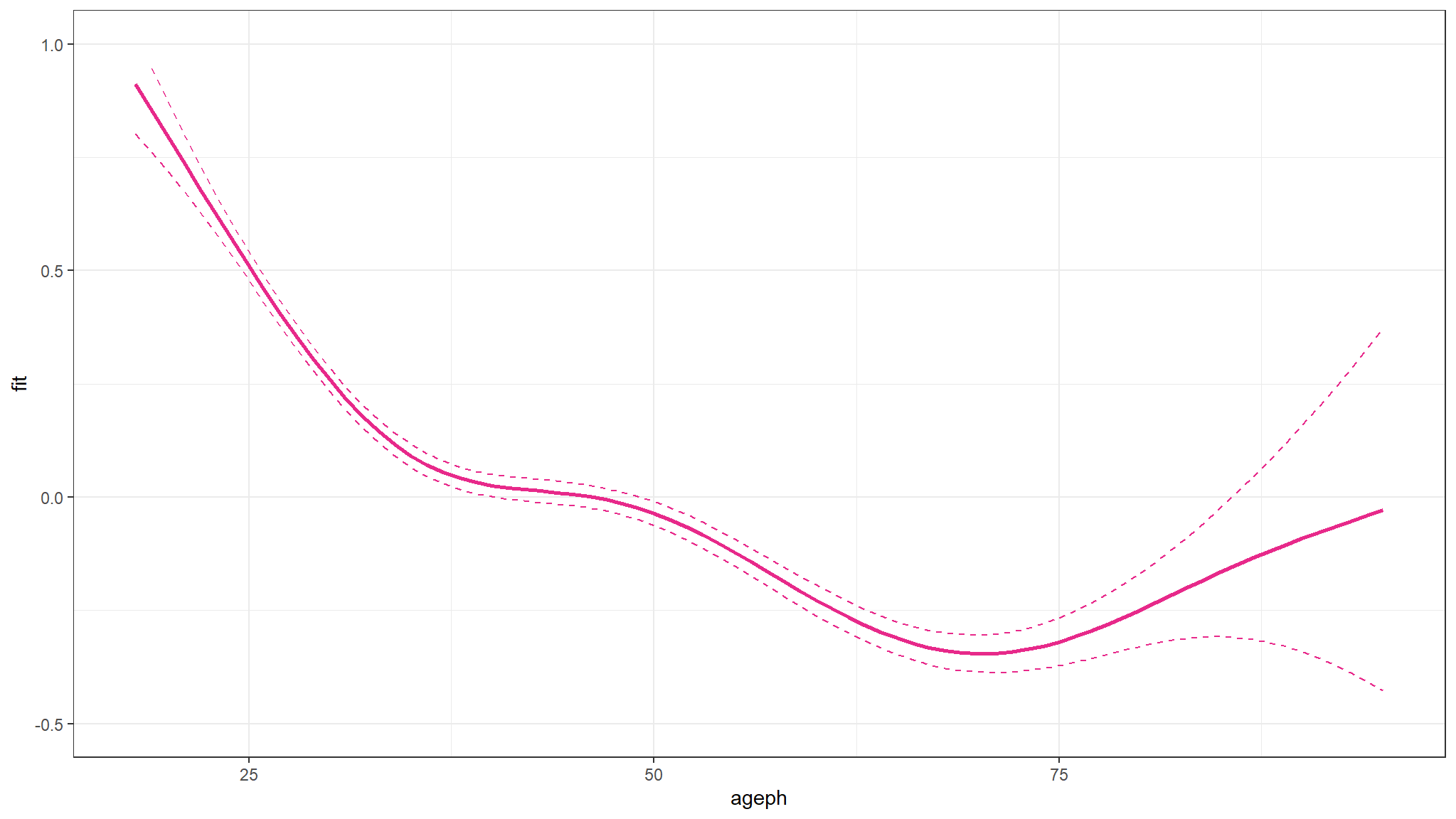

fitting a poison with a smooth function(age variable)!

#>

#> Family: poisson

#> Link function: log

#>

#> Formula:

#> nclaims ~ s(ageph)

#>

#> Parametric coefficients:

#> Estimate Std. Error z value Pr(>|z|)

#> (Intercept) -1.995268 0.007194 -277.3 <0.0000000000000002 ***

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#>

#> Approximate significance of smooth terms:

#> edf Ref.df Chi.sq p-value

#> s(ageph) 5.923 6.951 1390 <0.0000000000000002 ***

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#>

#> R-sq.(adj) = 0.00853 Deviance explained = 1.47%

#> UBRE = -0.45702 Scale est. = 1 n = 163231

Note

- the result shows that age is a significant smooth predictor of \(\mu\)

The figure shows that younger policyholders have a higher risk profile. The fitted GAM is lower than might be expected from the observed claim frequency for policyholders of age 19. This is because there are very few young policyholders of age 19 present in the portfolio.

prediction and prediction interval

Note

- again we would expect \(\mu\) to decrease with decreasing age

Effect of putting age into categories

- this allows to know exactly what happens in each category

- we attempt to determine weighted

(0%, 2.5%,10%,25%,50%,75%,90%,97.5%)quantiles of age and categorize the data in that order.

bins <- c(0,0.025,0.10,0.25,0.5,0.75,0.9,0.975,1)

split.Age <- wtd.quantile(out_dat$ageph,probs=bins)

split.Age

#> 0% 2.5% 10% 25% 50% 75% 90% 97.5% 100%

#> 18 24 28 35 46 58 68 76 95

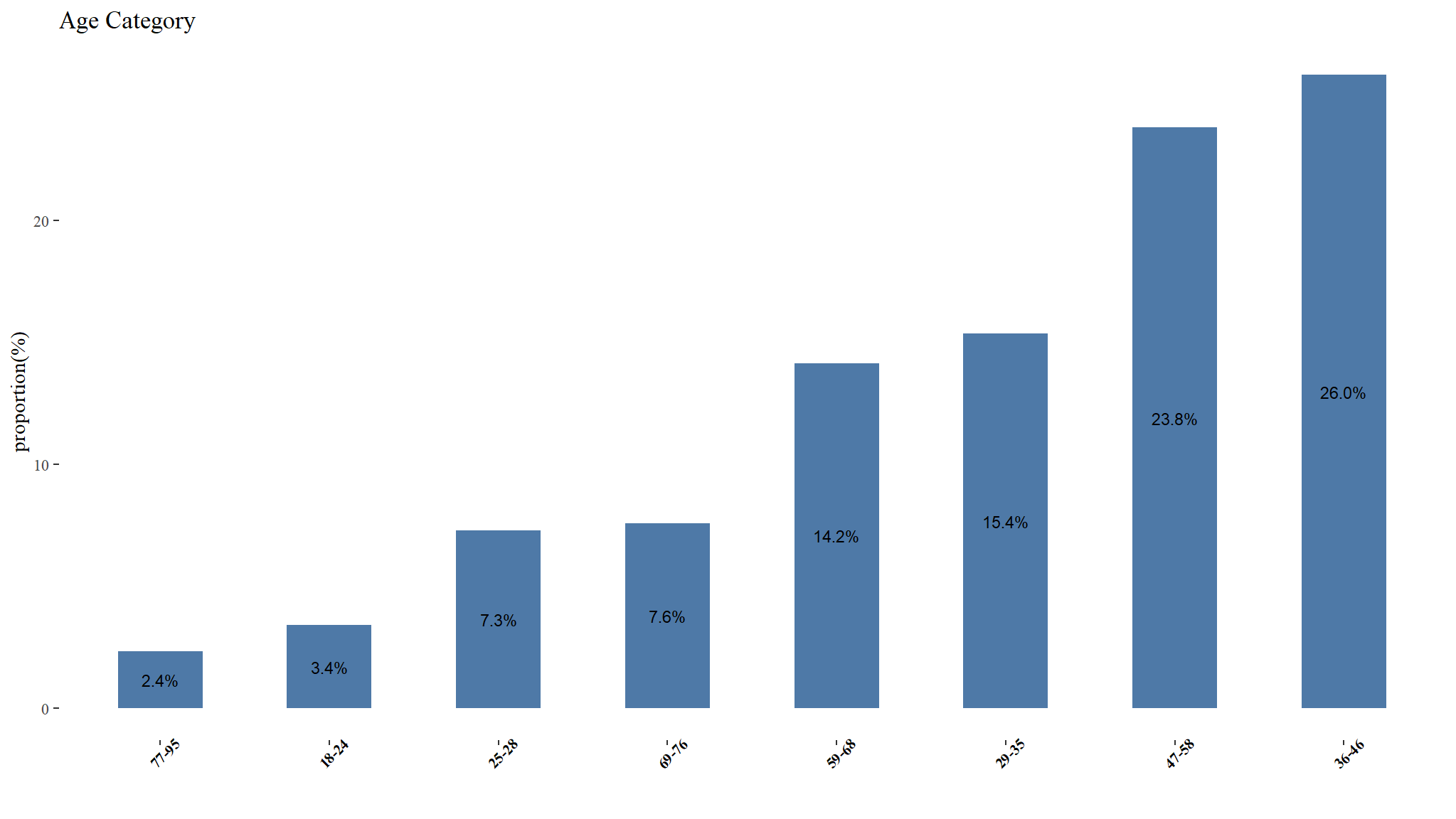

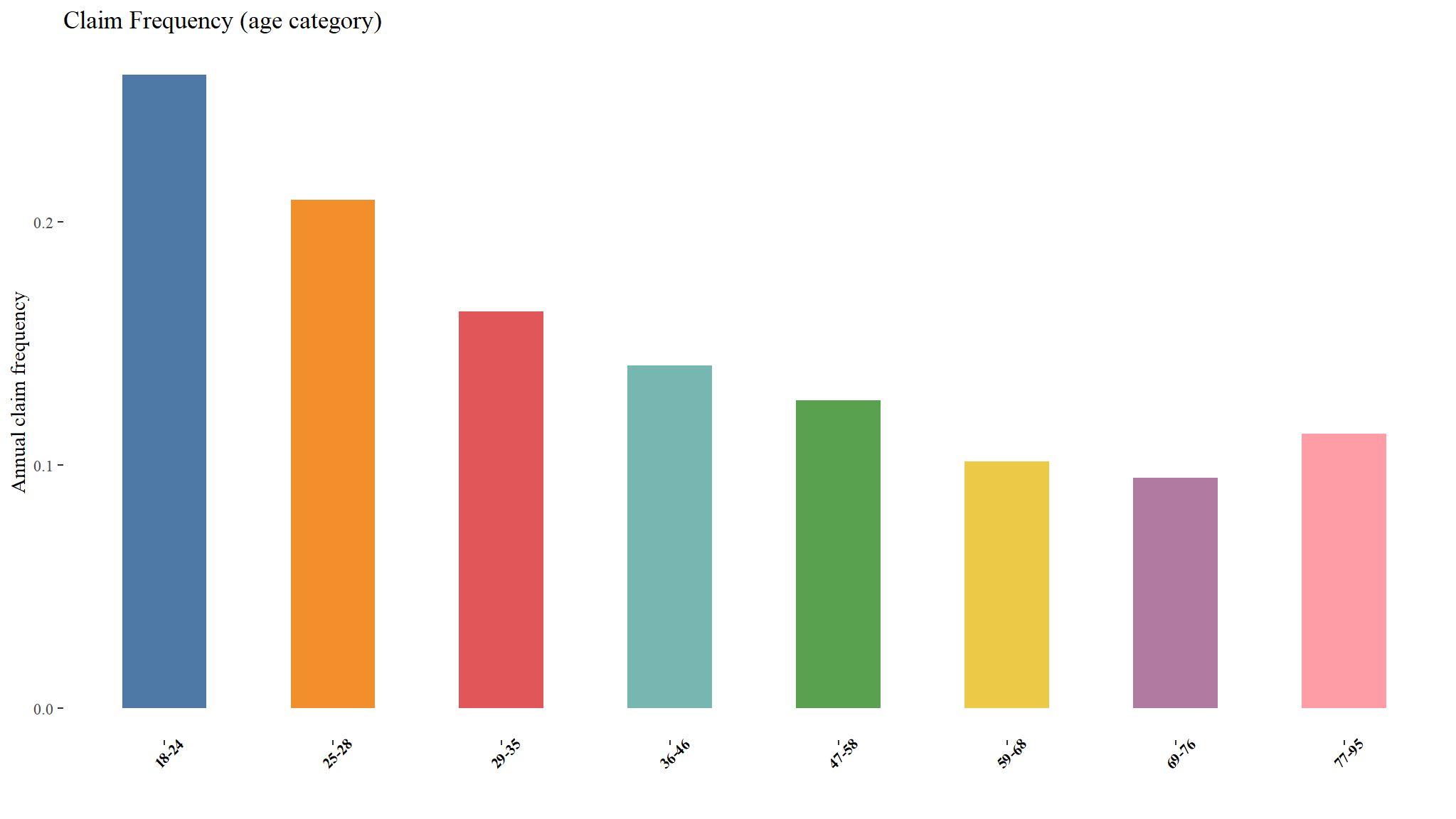

Risk classification for different age classes

out_dat %>%

group_by(age_cat) %>%

summarise(`emperical frequency` = sum(nclaims) / sum(exposure),

`total claims`=sum(nclaims),

count=n()) |>

knitr::kable(digits=3, "html", caption="Table : summary by age group") %>%

kable_styling("striped", "bordered") | age_cat | emperical frequency | total claims | count |

|---|---|---|---|

| 18-24 | 0.260 | 1231 | 5569 |

| 25-28 | 0.209 | 2165 | 11938 |

| 29-35 | 0.163 | 3521 | 25086 |

| 36-46 | 0.141 | 5236 | 42404 |

| 47-58 | 0.127 | 4429 | 38883 |

| 59-68 | 0.102 | 2152 | 23118 |

| 69-76 | 0.095 | 1101 | 12387 |

| 77-95 | 0.113 | 401 | 3846 |

Claim Frequency (age category)

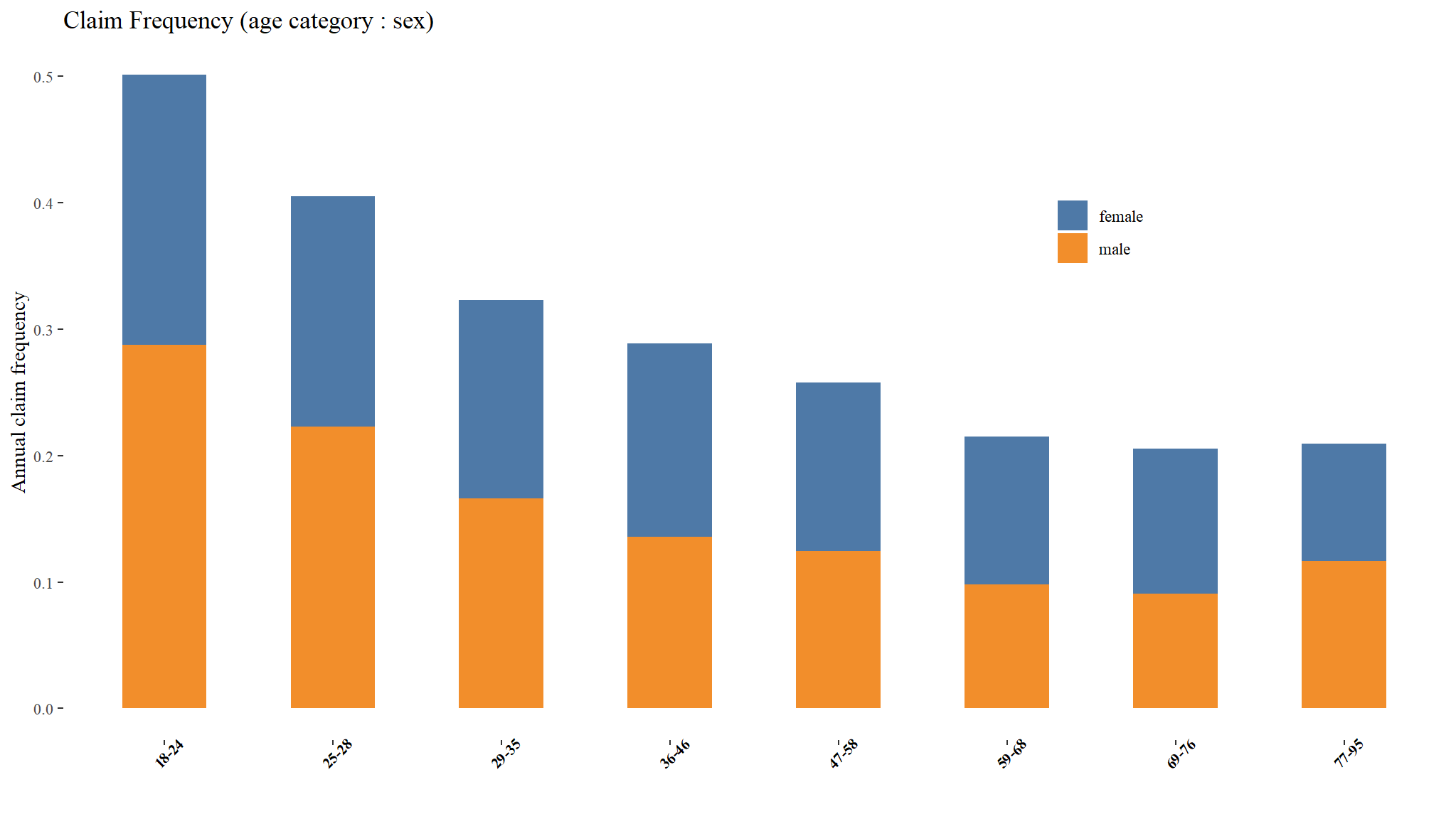

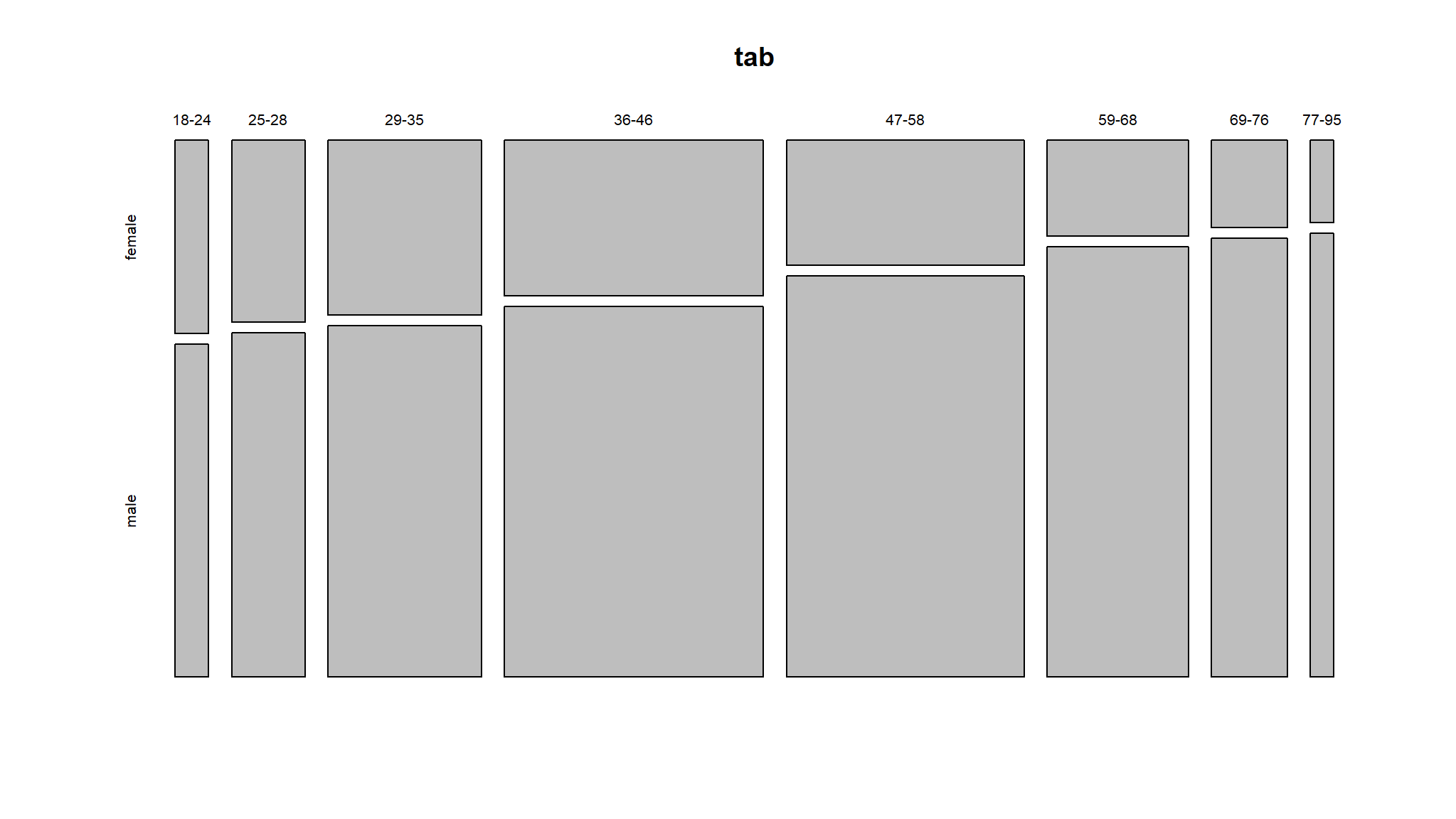

Risk classification: Possible interaction between age and sex?

out_dat %>%

group_by(sex,age_cat) %>%

summarise(`emperical frequency` = sum(nclaims) / sum(exposure),

`total claims`=sum(nclaims),

count=n()) |>

knitr::kable(digits=3, "html", caption="Table : summary by age group and sex") %>%

kable_styling("striped", "bordered") | sex | age_cat | emperical frequency | total claims | count |

|---|---|---|---|---|

| female | 18-24 | 0.214 | 372 | 2046 |

| female | 25-28 | 0.182 | 651 | 4133 |

| female | 29-35 | 0.157 | 1124 | 8325 |

| female | 36-46 | 0.153 | 1676 | 12556 |

| female | 47-58 | 0.133 | 1093 | 9244 |

| female | 59-68 | 0.117 | 448 | 4210 |

| female | 69-76 | 0.115 | 219 | 2057 |

| female | 77-95 | 0.093 | 51 | 604 |

| male | 18-24 | 0.287 | 859 | 3523 |

| male | 25-28 | 0.223 | 1514 | 7805 |

| male | 29-35 | 0.166 | 2397 | 16761 |

| male | 36-46 | 0.136 | 3560 | 29848 |

| male | 47-58 | 0.125 | 3336 | 29639 |

| male | 59-68 | 0.098 | 1704 | 18908 |

| male | 69-76 | 0.091 | 882 | 10330 |

| male | 77-95 | 0.116 | 350 | 3242 |

Claim Frequency (age category:sex)

- base R has a nice way of showing this

margin.table(tab,2)

#>

#> female male

#> 43175 120056We now create a model with age categorised

#>

#> Call:

#> glm(formula = nclaims ~ age_cat, family = poisson(link = "log"),

#> data = out_dat, offset = log(exposure))

#>

#> Coefficients:

#> Estimate Std. Error z value Pr(>|z|)

#> (Intercept) -1.34591 0.02850 -47.222 < 0.0000000000000002 ***

#> age_cat25-28 -0.21992 0.03570 -6.161 0.000000000724 ***

#> age_cat29-35 -0.46793 0.03311 -14.132 < 0.0000000000000002 ***

#> age_cat36-46 -0.61467 0.03168 -19.405 < 0.0000000000000002 ***

#> age_cat47-58 -0.72051 0.03222 -22.362 < 0.0000000000000002 ***

#> age_cat59-68 -0.94086 0.03574 -26.328 < 0.0000000000000002 ***

#> age_cat69-76 -1.01204 0.04148 -24.398 < 0.0000000000000002 ***

#> age_cat77-95 -0.83636 0.05750 -14.546 < 0.0000000000000002 ***

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#>

#> (Dispersion parameter for poisson family taken to be 1)

#>

#> Null deviance: 89944 on 163230 degrees of freedom

#> Residual deviance: 88666 on 163223 degrees of freedom

#> AIC: 126414

#>

#> Number of Fisher Scoring iterations: 6

comments

using the the simple output above we can say that ,the estimated claim frequency for each category are:

this implies that their claim frequency is 0.802583 fold(times) higher than the claim frequency of drivers in the reference category (18-24)

exp(-0.21992)

#> [1] 0.802583this implies that their claim frequency is 0.6262974 fold(times) higher than the claim frequency of drivers in the reference category (18-24)

exp(-0.46793)

#> [1] 0.6262974this implies that their claim frequency is 0.5408193 fold(times) higher than the claim frequency of drivers in the reference category (18-24)

exp(-0.61467)

#> [1] 0.5408193this implies that their claim frequency is 0.4865041 fold(times) higher than the claim frequency of drivers in the reference category (18-24)

exp(-0.72051)

#> [1] 0.4865041this implies that their claim frequency is 0.390292 fold(times) higher than the claim frequency of drivers in the reference category (18-24)

exp(-0.94086)

#> [1] 0.390292this implies that their claim frequency is 0.404898 fold(times) higher than the claim frequency of drivers in the reference category (18-24)

exp(-1.01204)

#> [1] 0.3634767this implies that their claim frequency is 0.4332848 fold(times) higher than the claim frequency of drivers in the reference category (18-24)

exp(-0.83636)

#> [1] 0.4332848

Generally

- we note that the

estimated claim frequencygenerally decreases going to higher age categories

tidy that a bit

| Characteristic | IRR1 | 95% CI1 | p-value |

|---|---|---|---|

| age_cat | |||

| 18-24 | — | — | |

| 25-28 | 0.80 | 0.75, 0.86 | <0.001 |

| 29-35 | 0.63 | 0.59, 0.67 | <0.001 |

| 36-46 | 0.54 | 0.51, 0.58 | <0.001 |

| 47-58 | 0.49 | 0.46, 0.52 | <0.001 |

| 59-68 | 0.39 | 0.36, 0.42 | <0.001 |

| 69-76 | 0.36 | 0.34, 0.39 | <0.001 |

| 77-95 | 0.43 | 0.39, 0.48 | <0.001 |

| 1 IRR = Incidence Rate Ratio, CI = Confidence Interval | |||

look at the prediction for this model

to add on

- the prediction plot is for those who have an exact exposure of 1 since this is the most frequent exposure value

- our prediction using the model suggests that as age increases , claim frequency decreases for individuals with an exposure value of

one

try a model with age and sex

#>

#> Call:

#> glm(formula = nclaims ~ age_cat + sex, family = poisson(link = "log"),

#> data = out_dat, offset = log(exposure))

#>

#> Coefficients:

#> Estimate Std. Error z value Pr(>|z|)

#> (Intercept) -1.33797 0.03019 -44.314 < 0.0000000000000002 ***

#> age_cat25-28 -0.21962 0.03570 -6.152 0.000000000765 ***

#> age_cat29-35 -0.46747 0.03312 -14.116 < 0.0000000000000002 ***

#> age_cat36-46 -0.61375 0.03170 -19.363 < 0.0000000000000002 ***

#> age_cat47-58 -0.71882 0.03229 -22.262 < 0.0000000000000002 ***

#> age_cat59-68 -0.93850 0.03586 -26.171 < 0.0000000000000002 ***

#> age_cat69-76 -1.00946 0.04161 -24.262 < 0.0000000000000002 ***

#> age_cat77-95 -0.83366 0.05760 -14.473 < 0.0000000000000002 ***

#> sexmale -0.01261 0.01584 -0.796 0.426

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#>

#> (Dispersion parameter for poisson family taken to be 1)

#>

#> Null deviance: 89944 on 163230 degrees of freedom

#> Residual deviance: 88666 on 163222 degrees of freedom

#> AIC: 126415

#>

#> Number of Fisher Scoring iterations: 6| Characteristic | IRR1 | 95% CI1 | p-value |

|---|---|---|---|

| age_cat | |||

| 18-24 | — | — | |

| 25-28 | 0.80 | 0.75, 0.86 | <0.001 |

| 29-35 | 0.63 | 0.59, 0.67 | <0.001 |

| 36-46 | 0.54 | 0.51, 0.58 | <0.001 |

| 47-58 | 0.49 | 0.46, 0.52 | <0.001 |

| 59-68 | 0.39 | 0.36, 0.42 | <0.001 |

| 69-76 | 0.36 | 0.34, 0.40 | <0.001 |

| 77-95 | 0.43 | 0.39, 0.49 | <0.001 |

| sex | |||

| female | — | — | |

| male | 0.99 | 0.96, 1.02 | 0.4 |

| 1 IRR = Incidence Rate Ratio, CI = Confidence Interval | |||

model building using AIC

freq_glm_full <- glm(nclaims ~ ageph+sex+coverage+use+fuel+fleet+pc+bm+power+agec, offset = log(exposure), data = out_dat, family = poisson(link = "log"))

MASS::stepAIC(freq_glm_full,direction="both")

#> Start: AIC=124988.1

#> nclaims ~ ageph + sex + coverage + use + fuel + fleet + pc +

#> bm + power + agec

#>

#> Df Deviance AIC

#> - agec 1 87233 124986

#> - sex 1 87234 124988

#> <none> 87233 124988

#> - use 1 87239 124992

#> - fleet 1 87241 124994

#> - coverage 2 87271 125022

#> - power 1 87324 125078

#> - pc 1 87350 125103

#> - fuel 1 87361 125115

#> - ageph 1 87446 125199

#> - bm 1 88464 126217

#>

#> Step: AIC=124986.5

#> nclaims ~ ageph + sex + coverage + use + fuel + fleet + pc +

#> bm + power

#>

#> Df Deviance AIC

#> - sex 1 87235 124986

#> <none> 87233 124986

#> + agec 1 87233 124988

#> - use 1 87239 124991

#> - fleet 1 87241 124993

#> - coverage 2 87275 125024

#> - power 1 87329 125080

#> - pc 1 87350 125102

#> - fuel 1 87365 125116

#> - ageph 1 87449 125200

#> - bm 1 88466 126217

#>

#> Step: AIC=124986.1

#> nclaims ~ ageph + coverage + use + fuel + fleet + pc + bm + power

#>

#> Df Deviance AIC

#> <none> 87235 124986

#> + sex 1 87233 124986

#> + agec 1 87234 124988

#> - use 1 87241 124990

#> - fleet 1 87243 124992

#> - coverage 2 87276 125023

#> - power 1 87329 125078

#> - pc 1 87353 125102

#> - fuel 1 87365 125114

#> - ageph 1 87458 125207

#> - bm 1 88474 126223

#>

#> Call: glm(formula = nclaims ~ ageph + coverage + use + fuel + fleet +

#> pc + bm + power, family = poisson(link = "log"), data = out_dat,

#> offset = log(exposure))

#>

#> Coefficients:

#> (Intercept) ageph coveragePO coverageTPL usework

#> -1.83493214 -0.00792846 -0.00037807 0.09498288 -0.08180670

#> fuelgasoline fleetY pc bm power

#> -0.17350485 -0.11981008 -0.00002857 0.06277044 0.00365499

#>

#> Degrees of Freedom: 163230 Total (i.e. Null); 163221 Residual

#> Null Deviance: 89940

#> Residual Deviance: 87230 AIC: 125000#>

#> Call:

#> glm(formula = nclaims ~ ageph + coverage + use + fuel + fleet +

#> pc + bm + power, family = poisson(link = "log"), data = out_dat,

#> offset = log(exposure))

#>

#> Coefficients:

#> Estimate Std. Error z value Pr(>|z|)

#> (Intercept) -1.834932140 0.043351298 -42.327 < 0.0000000000000002 ***

#> ageph -0.007928458 0.000536976 -14.765 < 0.0000000000000002 ***

#> coveragePO -0.000378075 0.023952053 -0.016 0.9874

#> coverageTPL 0.094982885 0.022089619 4.300 0.0000171 ***

#> usework -0.081806695 0.033446860 -2.446 0.0145 *

#> fuelgasoline -0.173504852 0.015079149 -11.506 < 0.0000000000000002 ***

#> fleetY -0.119810081 0.043512007 -2.753 0.0059 **

#> pc -0.000028574 0.000002633 -10.854 < 0.0000000000000002 ***

#> bm 0.062770436 0.001729931 36.285 < 0.0000000000000002 ***

#> power 0.003654994 0.000370316 9.870 < 0.0000000000000002 ***

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#>

#> (Dispersion parameter for poisson family taken to be 1)

#>

#> Null deviance: 89944 on 163230 degrees of freedom

#> Residual deviance: 87235 on 163221 degrees of freedom

#> AIC: 124986

#>

#> Number of Fisher Scoring iterations: 6| Characteristic | IRR1 | 95% CI1 | p-value |

|---|---|---|---|

| ageph | 0.99 | 0.99, 0.99 | <0.001 |

| coverage | |||

| FO | — | — | |

| PO | 1.00 | 0.95, 1.05 | >0.9 |

| TPL | 1.10 | 1.05, 1.15 | <0.001 |

| use | |||

| private | — | — | |

| work | 0.92 | 0.86, 0.98 | 0.014 |

| fuel | |||

| diesel | — | — | |

| gasoline | 0.84 | 0.82, 0.87 | <0.001 |

| fleet | |||

| N | — | — | |

| Y | 0.89 | 0.81, 0.97 | 0.006 |

| pc | 1.00 | 1.00, 1.00 | <0.001 |

| bm | 1.06 | 1.06, 1.07 | <0.001 |

| power | 1.00 | 1.00, 1.00 | <0.001 |

| 1 IRR = Incidence Rate Ratio, CI = Confidence Interval | |||